This example was automatically generated from a Jupyter notebook in the RxInferExamples.jl repository.

We welcome and encourage contributions! You can help by:

- Improving this example

- Creating new examples

- Reporting issues or bugs

- Suggesting enhancements

Visit our GitHub repository to get started. Together we can make RxInfer.jl even better! 💪

Contextual Bandits

We will start this notebook with a motivating example.

Let’s face it—ads are annoying. But very often they’re also one of the few ways to keep the business running. Imagine a free-to-play game for example. The real question isn’t whether to show ads, but when and which kind to show, so that players don’t feel bombarded, leave the game frustrated, or stop spending altogether.

It’s a balancing act between monetization and player retention.

If you show ads too aggressively, players quit. If you show ads too cautiously, you leave money on the table. So, how do you decide what to do in each moment of a player’s session?

Turning Ad Scheduling Into a Learning Problem

Every player session is different. Some players are engaged, some are rushing through, some just made a purchase, some are one level away from quitting.

At every possible ad moment, you have choices like:

- Show a video ad (high revenue, high interruption)

- Show a banner ad (low revenue, low interruption)

- Show no ad (defer to later)

And you have context—information about the session so far:

- Player’s level and progress

- Time since the last ad

- Time spent in the current session

- Whether the player just succeeded or failed at something

- Recent purchases or reward claims

What you want is a system that learns from player behavior over time, figuring out which actions perform best in which contexts—not just maximizing clicks or ad revenue right now, but balancing that with keeping players happy and playing longer.

Contextual Multi-Armed Bandits to the Rescue

This is exactly where Contextual Multi-Armed Bandits (CMABs) come in.

Contextual Multi‑Armed Bandits (CMABs) extend the classic bandit setting by allowing the learner to observe a context—a feature vector that describes the current situation—before selecting an action (or arm). The learner’s aim is to maximise cumulative reward over time by repeatedly balancing:

- Exploration – trying arms whose pay‑offs are still uncertain in some contexts.

- Exploitation – choosing the arm with the highest estimated reward in the current context.

CMABs sit between simple A/B tests and full reinforcement‑learning problems and are the work‑horse behind many personalisation engines.

Acting identically for every context wastes opportunity; CMABs formalise how to adapt decisions on‑the‑fly.

Implementing CMABs in RxInfer.jl

In this notebook we will implement a CMAB in RxInfer.jl way. A way to tackle CMAB in RxInfer requires expressing the generative model as a hierarchical Bayesian linear‑regression model and then message passing inference will do the rest.

Generative model (consistent notation)

Let

\[K\]

– number of arms.\[d\]

– dimension of the context vector.\[c_t\in\mathbb{R}^d\]

– context observed at round $t$.\[a_t\in{1,\dots,K}\]

– arm selected at round $t$.\[r_t\in\mathbb{R}\]

– realised reward.

The environment produces rewards according to:

- Global noise precision $\tau\;\sim\;\mathcal{G}(\alpha_\tau, \beta_\tau)$

- Arm‑specific regression parameters $k = 1,\dots,K$ $\theta_k \;\sim\; \mathcal{N}(m_{0k}, V_{0k}), \qquad \\ \Lambda_k \;\sim\; \operatorname{Wishart}(\nu_{0k}, W_{0k})$

- Per interaction latent coefficients $t = 1,\dots,T$ $\beta_t \;\sim\; \mathcal{N}(\theta_{a_t}, \Lambda_{a_t}^{-1})$

- Reward generation $\mu_t = c_t^\top \beta_t, \qquad \\ r_t \;\sim\; \mathcal{N}(\mu_t, \tau^{-1})$

Interpretation. Each arm owns a distribution of weight vectors ($\theta_k$), capturing how the context maps to reward for that arm. On every play we draw a concrete weight vector $\beta_t$, compute the expected reward $\mu_t$, and then observe a noisy realisation $r_t$.

Inference & decision‑making

With RxInfer we:

- Declare the model above with the

@modelmacro. (To make the example simpler, we'll have two models: one for parameters and one for predictions. A more complex scenario would be to have a single model for both.) - Stream incoming tuples $(c_t, a_t, r_t)$.

- Call

inferto update the posterior over $(\theta_k, \Lambda_k, \tau)$. - Compute predictive distributions of rewards in a new context $c_{t+1}$ via

inferon the predictive model: - Choose the next arm based on sampled from the predictive distribution.

Because both learning and prediction are expressed as probabilistic inference, we keep all uncertainty in closed form—ideal for principled exploration. The same pipeline generalises easily to non‑linear contexts (via feature maps) or non‑Gaussian rewards by swapping likelihood terms.

using RxInfer, Distributions, LinearAlgebra, Plots, StatsPlots, ProgressMeter, StableRNGs, RandomAt first let's generate synthetic data to simulate the CMAB problem.

using StableRNGs

# Random number generator

rng = StableRNG(42)

# Data generation parameters

n_train_samples = 300

n_test_samples = 100

n_total_samples = n_train_samples + n_test_samples

n_arms = 10

n_contexts = 50

context_dim = 20

noise_sd = 0.1

# Generate true arm parameters (θ_k in the model description)

arms = [randn(rng, context_dim) for _ in 1:n_arms]

# Generate context feature vectors with missing values

contexts = []

for i in 1:n_contexts

# Create a vector that can hold both Float64 and Missing values

context = Vector{Union{Float64,Missing}}(undef, context_dim)

# Fill with random values initially

for j in 1:context_dim

context[j] = randn(rng)

end

# Randomly introduce missing values in some contexts

if rand(rng) < 0.4 # 40% of contexts will have some missing values

n_missing = rand(rng, 1:2) # 1-2 missing values per context

# Simple approach: randomly select indices for missing values

missing_indices = []

while length(missing_indices) < n_missing

idx = rand(rng, 1:context_dim)

if !(idx in missing_indices)

push!(missing_indices, idx)

end

end

for idx in missing_indices

context[idx] = missing

end

end

push!(contexts, context)

end

# Synthetic reward function (reusable)

function compute_reward(arm_params, context_vec, noise_sd=0.0; rng=nothing)

"""

Compute reward for given arm parameters and context.

Args:

arm_params: Vector of arm parameters

context_vec: Context vector (may contain missing values)

noise_sd: Standard deviation of Gaussian noise to add

rng: Random number generator (optional, for reproducible noise)

Returns:

Scalar reward value

"""

# Calculate the deterministic part of the reward, handling missing values

mean_reward = 0.0

valid_dims = 0

for j in 1:length(context_vec)

if !ismissing(context_vec[j])

mean_reward += arm_params[j] * context_vec[j]

valid_dims += 1

end

end

# Normalize by the number of valid dimensions to maintain similar scale

if valid_dims > 0

mean_reward = mean_reward * (length(context_vec) / valid_dims)

end

# Add Gaussian noise if requested

if noise_sd > 0

if rng !== nothing

mean_reward += randn(rng) * noise_sd

else

mean_reward += randn() * noise_sd

end

end

return mean_reward

end

# Generate training and test data

function generate_bandit_data(n_samples, arms, contexts, noise_sd; rng, start_idx=1)

"""

Generate bandit data for given number of samples.

Returns:

(arm_choices, context_choices, rewards)

"""

arm_choices = []

context_choices = []

rewards = []

for i in 1:n_samples

# Randomly select a context and an arm

push!(context_choices, rand(rng, 1:length(contexts)))

push!(arm_choices, rand(rng, 1:length(arms)))

# Get the selected context and arm

selected_context = contexts[context_choices[end]]

selected_arm = arms[arm_choices[end]]

# Compute reward using the synthetic reward function

reward = compute_reward(selected_arm, selected_context, noise_sd; rng=rng)

push!(rewards, reward)

end

return arm_choices, context_choices, rewards

end

# Generate training data

println("Generating training data...")

train_arm_choices, train_context_choices, train_rewards = generate_bandit_data(

n_train_samples, arms, contexts, noise_sd; rng=rng

)

# Generate test data

println("Generating test data...")

test_arm_choices, test_context_choices, test_rewards = generate_bandit_data(

n_test_samples, arms, contexts, noise_sd; rng=rng

)

# Display information about the generated data

println("\nDataset Summary:")

println("Training samples: $n_train_samples")

println("Test samples: $n_test_samples")

println("Total contexts: $(length(contexts))")

println("Number of contexts with missing values: ", sum(any(ismissing, ctx) for ctx in contexts))

println("Arms: $n_arms")

println("Context dimension: $context_dim")

println("Noise standard deviation: $noise_sd")

# Show examples of contexts with missing values

println("\nExamples of contexts with missing values:")

count = 0

for (i, ctx) in enumerate(contexts)

if any(ismissing, ctx) && count < 3 # Show first 3 examples

println("Context $i: $ctx")

global count += 1

end

end

# Show sample data

println("\nTraining data samples (first 5):")

for i in 1:min(5, length(train_rewards))

println("Sample $i: Arm=$(train_arm_choices[i]), Context=$(train_context_choices[i]), Reward=$(round(train_rewards[i], digits=4))")

end

println("\nTest data samples (first 5):")

for i in 1:min(5, length(test_rewards))

println("Sample $i: Arm=$(test_arm_choices[i]), Context=$(test_context_choices[i]), Reward=$(round(test_rewards[i], digits=4))")

end

# Verify the reward function works correctly

println("\nTesting reward function:")

test_context = contexts[1]

test_arm = arms[1]

deterministic_reward = compute_reward(test_arm, test_context, 0.0) # No noise

noisy_reward = compute_reward(test_arm, test_context, noise_sd; rng=rng) # With noise

println("Deterministic reward: $(round(deterministic_reward, digits=4))")

println("Noisy reward: $(round(noisy_reward, digits=4))")Generating training data...

Generating test data...

Dataset Summary:

Training samples: 300

Test samples: 100

Total contexts: 50

Number of contexts with missing values: 22

Arms: 10

Context dimension: 20

Noise standard deviation: 0.1

Examples of contexts with missing values:

Context 3: Union{Missing, Float64}[missing, -0.4741385118651381, -1.0989041

9081401, -1.079288892379018, 0.8184199040107111, -0.30409464242950546, -0.6

709508997562322, -0.7469592378369052, 0.21407501633089995, -0.6139813001136

504, 2.8170273653049507, -1.4362435690909499, -0.30112508107598307, -0.3868

83090487843, 0.6563571763621648, 1.401591444397142, 0.6193863742347839, 0.1

2760715013378465, -0.2758495479700435, 1.8822768045661076]

Context 8: Union{Missing, Float64}[-2.3650237776747054, -1.1739461025984783

, 1.128284045692684, -0.8690689832066373, 0.4497591893001418, -0.2617237965

612964, 0.07868265261314639, missing, 1.9119126287271901, 0.719828217704402

8, -2.708690227134825, -2.645555311022844, -0.3202946667428825, 1.398258591

17344, 0.06974735851443013, 1.1639494445584129, -0.36687387238833036, 0.506

2972107773495, -1.3675557327045547, missing]

Context 9: Union{Missing, Float64}[-0.7928407885849085, 0.5230893424666117,

0.21944291871653826, -0.2951043978830045, missing, 0.6739591611416778, 0.6

091981160535558, 0.37661376790321904, -0.08201072963796563, 0.6762611326141

408, -1.7998621684347569, 0.7079334064897562, -1.5082653360123872, 0.423324

15672698104, 1.380447484940245, -3.325041477189219, 1.1893655835458625, 0.9

25128468276957, -1.62673585658528, -0.667629748025382]

Training data samples (first 5):

Sample 1: Arm=6, Context=11, Reward=2.7556

Sample 2: Arm=2, Context=14, Reward=-3.911

Sample 3: Arm=8, Context=14, Reward=-2.0472

Sample 4: Arm=6, Context=36, Reward=9.6666

Sample 5: Arm=3, Context=21, Reward=-4.1496

Test data samples (first 5):

Sample 1: Arm=1, Context=18, Reward=0.3271

Sample 2: Arm=2, Context=27, Reward=-3.2327

Sample 3: Arm=4, Context=4, Reward=-2.1027

Sample 4: Arm=1, Context=7, Reward=4.7518

Sample 5: Arm=8, Context=24, Reward=3.4953

Testing reward function:

Deterministic reward: -2.2755

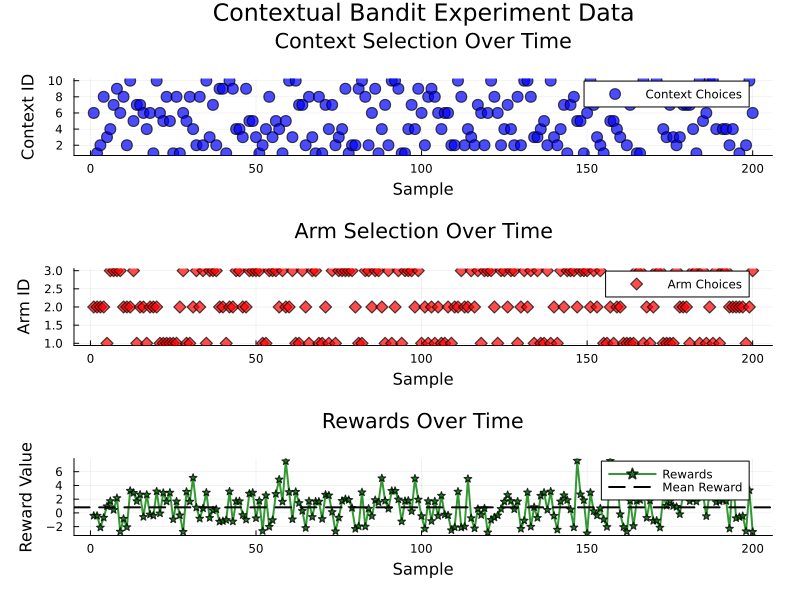

Noisy reward: -2.2613function create_bandit_plots(arm_choices, context_choices, rewards, title_prefix, color_scheme)

p1 = scatter(1:length(context_choices), context_choices,

label="Context Choices",

title="$title_prefix: Context Selection",

xlabel="Sample", ylabel="Context ID",

marker=:circle, markersize=6,

color=color_scheme[:context], alpha=0.7)

p2 = scatter(1:length(arm_choices), arm_choices,

label="Arm Choices",

title="$title_prefix: Arm Selection",

xlabel="Sample", ylabel="Arm ID",

marker=:diamond, markersize=6,

color=color_scheme[:arm], alpha=0.7)

p3 = plot(1:length(rewards), rewards,

label="Rewards",

title="$title_prefix: Rewards",

xlabel="Sample", ylabel="Reward Value",

linewidth=2, marker=:star, markersize=4,

color=color_scheme[:reward], alpha=0.8)

hline!(p3, [mean(rewards)], label="Mean Reward",

linestyle=:dash, linewidth=2, color=:black)

return plot(p1, p2, p3, layout=(3, 1), size=(800, 600))

end

# Create training plots

train_colors = Dict(:context => :blue, :arm => :red, :reward => :green)

train_plot = create_bandit_plots(train_arm_choices, train_context_choices, train_rewards,

"Training Data", train_colors)

# Create test plots

test_colors = Dict(:context => :lightblue, :arm => :pink, :reward => :lightgreen)

test_plot = create_bandit_plots(test_arm_choices, test_context_choices, test_rewards,

"Test Data", test_colors)

# Display both

plot(train_plot, test_plot, layout=(1, 2), size=(1600, 600),

plot_title="Contextual Bandit Experiment: Training and Test Data")

@model function conditional_regression(n_arms, priors, past_rewards, past_choices, past_contexts)

local θ

local γ

local τ

# Prior for each arm's parameters

for k in 1:n_arms

θ[k] ~ priors[:θ][k]

γ[k] ~ priors[:γ][k]

end

# Prior for the noise precision

τ ~ priors[:τ]

# Model for past observations

for n in eachindex(past_rewards)

arm_vals[n] ~ NormalMixture(switch=past_choices[n], m=θ, p=γ)

latent_context[n] ~ past_contexts[n]

past_rewards[n] ~ softdot(arm_vals[n], latent_context[n], τ)

end

endLet's define the priors.

priors_rng = StableRNG(42)

priors = Dict(

:θ => [MvNormalMeanPrecision(randn(priors_rng, context_dim), diagm(ones(context_dim))) for _ in 1:n_arms],

:γ => [Wishart(context_dim + 1, diagm(ones(context_dim))) for _ in 1:n_arms],

:τ => GammaShapeRate(1.0, 1.0)

)Dict{Symbol, Any} with 3 entries:

:γ => Wishart{Float64, PDMat{Float64, Matrix{Float64}}, Int64}[Distributi

ons.…

:τ => ExponentialFamily.GammaShapeRate{Float64}(a=1.0, b=1.0)

:θ => MvNormalMeanPrecision{Float64, Vector{Float64}, Matrix{Float64}}[Mv

Norm…And finally run the inference.

function run_inference(; n_arms, priors, past_rewards, past_choices, past_contexts, iterations=50, free_energy=true)

init = @initialization begin

q(θ) = priors[:θ]

q(γ) = priors[:γ]

q(τ) = priors[:τ]

q(latent_context) = MvNormalMeanPrecision(zeros(context_dim), Diagonal(ones(context_dim)))

end

return infer(

model=conditional_regression(

n_arms=n_arms,

priors=priors,

past_contexts=past_contexts,

),

data=(

past_rewards=past_rewards,

past_choices=past_choices,

),

constraints=MeanField(),

initialization=init,

showprogress=true,

iterations=iterations,

free_energy=free_energy

)

endrun_inference (generic function with 1 method)# Utility function to convert context with missing values to MvNormal distribution

function context_to_mvnormal(context_vec; tiny_precision=1e-6, huge_precision=1e6)

"""

Convert a context vector (potentially with missing values) to MvNormal distribution.

Args:

context_vec: Vector that may contain missing values

tiny_v: Small variance for known values (high precision)

huge_var: Large variance for missing values (low precision)

Returns:

MvNormal distribution

"""

context_mean = Vector{Float64}(undef, length(context_vec))

context_precision = Vector{Float64}(undef, length(context_vec))

for j in 1:length(context_vec)

if ismissing(context_vec[j])

context_mean[j] = 0.0

context_precision[j] = tiny_precision

else

context_mean[j] = context_vec[j]

context_precision[j] = huge_precision

end

end

return MvNormalMeanPrecision(context_mean, Diagonal(context_precision))

endcontext_to_mvnormal (generic function with 1 method)# Convert to the required types for the model (TRAINING DATA ONLY)

rewards_data = Float64.(train_rewards)

# Parameters for the covariance matrix

tiny_precision = 1e-6 # Very high precision (small variance) for known values

huge_precision = 1e6 # Very low precision (large variance) for missing values

contexts_data = [

let context = contexts[idx]

context_to_mvnormal(context; tiny_precision=tiny_precision, huge_precision=huge_precision)

end

for idx in train_context_choices # Use training context choices

]

arm_choices_data = [[Float64(k == chosen_arm) for k in 1:n_arms] for chosen_arm in train_arm_choices]; # Use training arm choicesresult = run_inference(

n_arms=n_arms,

priors=priors,

past_rewards=rewards_data,

past_choices=arm_choices_data,

past_contexts=contexts_data,

iterations=20,

free_energy=false

)Inference results:

Posteriors | available for (γ, arm_vals, τ, latent_context, θ)# Diagnostics of inferred arms

# 1. MSE of inferred arms coefficients

inferred_arms = mean.(result.posteriors[:θ][end])

mse_arms = mean(mean((inferred_arms[i] .- arms[i]) .^ 2) for i in eachindex(arms))

println("MSE of inferred arm coefficients: $mse_arms")MSE of inferred arm coefficients: 0.005138753286482585# Function to compute predicted rewards using softdot rules

function compute_predicted_rewards_with_variance(

arm_posteriors,

precision_posterior,

eval_arm_choices,

eval_context_choices,

eval_rewards

)

predicted_rewards = []

reward_variances = []

for i in 1:length(eval_rewards) # Evaluate on all samples in the evaluation set

arm_idx = eval_arm_choices[i]

ctx_idx = eval_context_choices[i]

# Get the posterior distributions

q_arm = arm_posteriors[arm_idx] # Posterior over arm parameters

q_precision = precision_posterior # Precision posterior

# Get the actual context and convert to MvNormal

actual_context = contexts[ctx_idx]

q_context = context_to_mvnormal(actual_context)

# Use softdot rule to compute predicted reward distribution

predicted_reward_dist = NormalMeanPrecision(

mean(q_arm)' * mean(q_context),

mean(q_precision)

)

push!(predicted_rewards, mean(predicted_reward_dist))

push!(reward_variances, var(predicted_reward_dist))

end

return predicted_rewards, reward_variances

end

# Function to display evaluation results

function display_evaluation_results(predicted_rewards, reward_variances, actual_rewards,

arm_choices, context_choices, dataset_name)

println("\n$dataset_name Evaluation Results:")

println("Sample | Actual Reward | Predicted Mean | Predicted Std | Arm | Context")

println("-------|---------------|----------------|---------------|-----|--------")

for i in 1:min(10, length(predicted_rewards))

actual = actual_rewards[i]

pred_mean = predicted_rewards[i]

pred_std = sqrt(reward_variances[i])

arm_idx = arm_choices[i]

ctx_idx = context_choices[i]

println("$(lpad(i, 6)) | $(rpad(round(actual, digits=4), 13)) | $(rpad(round(pred_mean, digits=4), 14)) | $(rpad(round(pred_std, digits=4), 13)) | $(lpad(arm_idx, 3)) | $(lpad(ctx_idx, 7))")

end

# Compute prediction metrics

prediction_mse = mean((predicted_rewards .- actual_rewards) .^ 2)

println("\n$dataset_name Prediction MSE: $prediction_mse")

# Compute log-likelihood of actual rewards under predicted distributions

log_likelihood = sum(

logpdf(Normal(predicted_rewards[i], sqrt(reward_variances[i])), actual_rewards[i])

for i in 1:length(predicted_rewards)

)

println("$dataset_name Average log-likelihood: $(log_likelihood / length(predicted_rewards))")

return prediction_mse, log_likelihood / length(predicted_rewards)

end

# Evaluate on TRAINING data

println("=== TRAINING DATA EVALUATION ===")

train_predicted_rewards, train_reward_variances = compute_predicted_rewards_with_variance(

result.posteriors[:θ][end], # Use full posteriors

result.posteriors[:τ][end], # Precision posterior

train_arm_choices,

train_context_choices,

train_rewards

)

train_mse, train_ll = display_evaluation_results(

train_predicted_rewards,

train_reward_variances,

train_rewards,

train_arm_choices,

train_context_choices,

"Training"

)

# Evaluate on TEST data

println("\n=== TEST DATA EVALUATION ===")

test_predicted_rewards, test_reward_variances = compute_predicted_rewards_with_variance(

result.posteriors[:θ][end], # Use full posteriors

result.posteriors[:τ][end], # Precision posterior

test_arm_choices,

test_context_choices,

test_rewards

)

test_mse, test_ll = display_evaluation_results(

test_predicted_rewards,

test_reward_variances,

test_rewards,

test_arm_choices,

test_context_choices,

"Test"

)

# Summary comparison

println("\n=== SUMMARY COMPARISON ===")

println("Dataset | MSE | Log-Likelihood")

println("-----------|----------|---------------")

println("Training | $(rpad(round(train_mse, digits=4), 8)) | $(round(train_ll, digits=4))")

println("Test | $(rpad(round(test_mse, digits=4), 8)) | $(round(test_ll, digits=4))")

if test_mse > train_mse * 1.2

println("\nNote: Test MSE is significantly higher than training MSE - possible overfitting")

elseif test_mse < train_mse * 0.8

println("\nNote: Test MSE is lower than training MSE - good generalization!")

else

println("\nNote: Test and training performance are similar - good generalization")

end=== TRAINING DATA EVALUATION ===

Training Evaluation Results:

Sample | Actual Reward | Predicted Mean | Predicted Std | Arm | Context

-------|---------------|----------------|---------------|-----|--------

1 | 2.7556 | 2.7721 | 1.3082 | 6 | 11

2 | -3.911 | -3.535 | 1.3082 | 2 | 14

3 | -2.0472 | -1.8887 | 1.3082 | 8 | 14

4 | 9.6666 | 8.1026 | 1.3082 | 6 | 36

5 | -4.1496 | -3.8266 | 1.3082 | 3 | 21

6 | -4.7496 | -4.5237 | 1.3082 | 4 | 49

7 | -2.1116 | -2.1877 | 1.3082 | 5 | 34

8 | 0.3173 | 0.5183 | 1.3082 | 8 | 32

9 | -4.9155 | -4.1394 | 1.3082 | 8 | 49

10 | -3.0535 | -3.3429 | 1.3082 | 6 | 31

Training Prediction MSE: 0.16609598579011065

Training Average log-likelihood: -1.236149219320253

=== TEST DATA EVALUATION ===

Test Evaluation Results:

Sample | Actual Reward | Predicted Mean | Predicted Std | Arm | Context

-------|---------------|----------------|---------------|-----|--------

1 | 0.3271 | 0.0431 | 1.3082 | 1 | 18

2 | -3.2327 | -2.6156 | 1.3082 | 2 | 27

3 | -2.1027 | -1.8232 | 1.3082 | 4 | 4

4 | 4.7518 | 4.465 | 1.3082 | 1 | 7

5 | 3.4953 | 2.9212 | 1.3082 | 8 | 24

6 | 1.0455 | 0.3028 | 1.3082 | 4 | 15

7 | -0.2608 | -0.2963 | 1.3082 | 9 | 38

8 | -6.0007 | -5.6078 | 1.3082 | 8 | 1

9 | -3.1662 | -2.8644 | 1.3082 | 7 | 36

10 | 0.9946 | 1.1453 | 1.3082 | 10 | 24

Test Prediction MSE: 0.17808283508293526

Test Average log-likelihood: -1.2396510580518532

=== SUMMARY COMPARISON ===

Dataset | MSE | Log-Likelihood

-----------|----------|---------------

Training | 0.1661 | -1.2361

Test | 0.1781 | -1.2397

Note: Test and training performance are similar - good generalization# Additional diagnostics

println("\n=== ADDITIONAL DIAGNOSTICS ===")

# Show precision/variance information

precision_posterior = result.posteriors[:τ][end]

println("Inferred noise precision: mean=$(round(mean(precision_posterior), digits=4)), " *

"std=$(round(std(precision_posterior), digits=4))")

println("Inferred noise variance: $(round(1/mean(precision_posterior), digits=4))")

println("True noise variance: $(round(noise_sd^2, digits=4))")

# Show arm coefficient statistics

println("\nArm coefficient comparison:")

for i in eachindex(arms)

true_arm = arms[i]

inferred_arm_posterior = result.posteriors[:θ][end][i]

inferred_arm_mean = mean(inferred_arm_posterior)

println("Arm $i:")

println(" True: $(round.(true_arm, digits=3))")

println(" Inferred: $(round.(inferred_arm_mean, digits=3))")

println(" MSE: $(round(mean((inferred_arm_mean .- true_arm).^2), digits=4))")

end

println("\nNumber of contexts with missing values: ", sum(any(ismissing, ctx) for ctx in contexts))=== ADDITIONAL DIAGNOSTICS ===

Inferred noise precision: mean=0.5843, std=0.0475

Inferred noise variance: 1.7115

True noise variance: 0.01

Arm coefficient comparison:

Arm 1:

True: [-0.67, 0.447, 1.374, 1.31, 0.126, 0.684, -1.019, -0.794, 1.775

, 1.297, -1.644, 0.794, -1.31, -0.037, 1.072, -0.397, -0.239, -0.651, 1.134

, -0.84]

Inferred: [-0.604, 0.429, 1.306, 1.212, 0.094, 0.665, -0.972, -0.744, 1.6

85, 1.264, -1.578, 0.765, -1.279, -0.01, 1.043, -0.381, -0.209, -0.582, 1.0

56, -0.76]

MSE: 0.003

Arm 2:

True: [2.085, -1.801, 0.483, -0.57, -0.665, 2.243, -1.464, -1.012, -2

.042, -0.787, 0.591, 0.642, 0.455, 0.054, 0.288, 0.587, -1.694, -0.696, -0.

301, 2.101]

Inferred: [1.997, -1.708, 0.451, -0.542, -0.636, 2.161, -1.364, -0.965, -

1.964, -0.754, 0.49, 0.614, 0.459, 0.044, 0.171, 0.557, -1.624, -0.59, -0.1

67, 2.001]

MSE: 0.0057

Arm 3:

True: [-0.69, -0.73, -1.417, -1.383, 1.201, 0.576, -0.987, 0.626, 0.1

87, 0.239, -1.287, 0.147, -0.345, 1.909, 0.093, -0.643, 0.743, 0.725, 0.077

, -0.008]

Inferred: [-0.655, -0.724, -1.353, -1.319, 1.132, 0.548, -0.898, 0.526, 0

.194, 0.232, -1.263, 0.115, -0.257, 1.834, 0.068, -0.568, 0.703, 0.694, 0.0

66, 0.001]

MSE: 0.0029

Arm 4:

True: [-0.37, 0.888, -1.056, 1.242, 0.628, 1.161, -0.851, -0.428, 0.1

09, -1.932, 0.105, 0.016, 0.105, 1.434, 0.141, 1.295, -0.931, 1.076, -1.799

, -0.822]

Inferred: [-0.23, 0.849, -1.04, 1.172, 0.477, 1.134, -0.779, -0.355, 0.12

8, -1.876, 0.097, 0.068, 0.037, 1.372, 0.124, 1.243, -0.905, 1.014, -1.727,

-0.796]

MSE: 0.0044

Arm 5:

True: [-0.217, 0.641, -1.566, -1.487, -0.45, -0.937, -0.59, 1.572, -0

.229, 0.473, 2.148, -0.614, -0.451, -1.672, -0.224, 0.461, -0.093, 1.038, -

1.827, 0.698]

Inferred: [-0.201, 0.628, -1.515, -1.422, -0.373, -0.907, -0.495, 1.468,

-0.22, 0.476, 2.079, -0.564, -0.238, -1.613, -0.101, 0.433, -0.104, 0.973,

-1.731, 0.634]

MSE: 0.0062

Arm 6:

True: [0.403, 0.333, 1.549, 0.156, 1.816, -0.626, -1.275, 0.485, 1.23

5, -1.121, -1.397, -0.658, -1.516, -0.712, -0.411, -1.254, 2.082, -0.53, -1

.64, -0.769]

Inferred: [0.227, 0.312, 1.496, 0.107, 1.705, -0.594, -1.151, 0.383, 1.17

4, -1.069, -1.351, -0.631, -1.445, -0.645, -0.4, -1.167, 2.001, -0.41, -1.5

89, -0.716]

MSE: 0.0064

Arm 7:

True: [1.528, 0.269, 1.215, 0.067, 0.84, 0.819, -1.459, 0.689, -1.067

, 1.278, -0.364, -1.031, -0.452, -1.973, 0.266, 0.212, -0.424, -1.286, 0.57

5, 0.72]

Inferred: [1.427, 0.271, 1.184, 0.041, 0.669, 0.79, -1.354, 0.645, -1.021

, 1.246, -0.335, -0.992, -0.375, -1.893, 0.271, 0.224, -0.355, -1.19, 0.552

, 0.696]

MSE: 0.0044

Arm 8:

True: [-0.651, -1.01, -0.863, 1.512, 0.743, -1.477, -0.288, -0.288, -

0.496, -0.151, 0.53, -0.429, -1.288, 0.95, 2.584, 0.719, -0.205, 1.232, -1.

135, -0.626]

Inferred: [-0.581, -0.964, -0.852, 1.411, 0.673, -1.425, -0.219, -0.262,

-0.466, -0.11, 0.486, -0.396, -1.228, 0.854, 2.469, 0.685, -0.191, 1.095, -

1.062, -0.546]

MSE: 0.0047

Arm 9:

True: [-1.049, 2.431, -0.434, 0.316, 1.271, -0.947, 0.131, 0.423, 0.1

62, -1.648, -0.058, -0.573, 1.01, -0.237, 0.212, -0.347, 0.143, -1.574, 0.7

96, 0.944]

Inferred: [-1.0, 2.341, -0.415, 0.143, 1.223, -0.91, 0.113, 0.439, 0.094,

-1.557, -0.066, -0.531, 0.986, -0.146, 0.122, -0.118, 0.131, -1.518, 0.769

, 0.869]

MSE: 0.0069

Arm 10:

True: [0.447, -1.369, 0.6, 0.392, -0.449, 0.049, -0.558, -1.213, -0.2

44, -0.289, 0.85, -0.834, 0.803, 1.531, -0.387, -1.258, -1.299, -1.05, -0.2

37, 0.536]

Inferred: [0.368, -1.322, 0.586, 0.295, -0.191, 0.04, -0.502, -1.155, -0.

24, -0.256, 0.813, -0.81, 0.782, 1.47, -0.29, -1.197, -1.278, -0.936, -0.14

6, 0.505]

MSE: 0.0067

Number of contexts with missing values: 22Comparing Different Strategies for the Contextual Bandit Problem

We'll implement and evaluate three different approaches:

- Random Strategy - Selecting arms randomly without using context information

- Vanilla Thompson Sampling - Sampling the reward distribution

- RxInfer Predictive Inference - Approximating the predictive posterior via message-passing

function random_strategy(; rng, n_arms)

chosen_arm = rand(rng, 1:n_arms)

return chosen_arm

end

function thompson_strategy(; rng, n_arms, current_context, posteriors)

# Thompson Sampling: Sample parameter vectors and choose best arm

expected_rewards = zeros(n_arms)

for k in 1:n_arms

# Sample parameters from posterior

theta_sample = rand(rng, posteriors[:θ][k])

# context might have missing values, so we use the mean of the context

augmented_context = mean(context_to_mvnormal(current_context))

expected_rewards[k] = dot(theta_sample, augmented_context)

end

# Choose best arm based on sampled parameters

chosen_arm = argmax(expected_rewards)

return chosen_arm

endthompson_strategy (generic function with 1 method)@model function contextual_bandit_predictive(reward, priors, current_context)

local θ

local γ

local τ

# Prior for each arm's parameters

for k in 1:n_arms

θ[k] ~ priors[:θ][k]

γ[k] ~ priors[:γ][k]

end

τ ~ priors[:τ]

chosen_arm ~ Categorical(ones(n_arms) ./ n_arms)

arm_vals ~ NormalMixture(switch=chosen_arm, m=θ, p=γ)

latent_context ~ current_context

reward ~ softdot(arm_vals, latent_context, τ)

end

function predictive_strategy(; rng, n_arms, current_context, posteriors)

priors = Dict(

:θ => posteriors[:θ],

:γ => posteriors[:γ],

:τ => posteriors[:τ]

)

latent_context = context_to_mvnormal(current_context)

init = @initialization begin

q(θ) = priors[:θ]

q(τ) = priors[:τ]

q(γ) = priors[:γ]

q(latent_context) = latent_context

q(chosen_arm) = Categorical(ones(n_arms) ./ n_arms)

end

result = infer(

model=contextual_bandit_predictive(

priors=priors,

current_context=latent_context

),

data=(reward=10maximum(train_rewards),),

constraints=MeanField(),

initialization=init,

showprogress=true,

iterations=20,

)

chosen_arm = argmax(probvec(result.posteriors[:chosen_arm][end]))

return chosen_arm

endpredictive_strategy (generic function with 1 method)As we defined the strategies, we can proceed to defining the helper functions to run the simulation.

We will use the following flow:

- PLAN - Run different strategies

- ACT - In this simulation, we're evaluating all strategies in parallel

- OBSERVE - Get rewards for all strategies

- LEARN - Update posteriors based on history

- KEEP HISTORY - Record all results

# Helper functions

function select_context(rng, n_contexts)

idx = rand(rng, 1:n_contexts)

return (index=idx, value=contexts[idx])

end

function plan(rng, n_arms, context, posteriors)

# Generate actions from different strategies

return Dict(

:random => random_strategy(rng=rng, n_arms=n_arms),

:thompson => thompson_strategy(rng=rng, n_arms=n_arms, current_context=context, posteriors=posteriors),

:predictive => predictive_strategy(rng=rng, n_arms=n_arms, current_context=context, posteriors=posteriors)

)

end

function act(rng, strategies)

# Here one would choose which strategy to actually follow

# For this simulation, we're evaluating all in parallel

# In a real scenario, one might return just one: return strategies[:thompson]

return strategies

end

function observe(rng, strategies, context, arms, noise_sd)

rewards = Dict()

for (strategy, arm_idx) in strategies

rewards[strategy] = compute_reward(arms[arm_idx], context, noise_sd)

end

return rewards

end

function learn(rng, n_arms, posteriors, past_rewards, past_choices, past_contexts)

# Note that we don't do any forgetting here which might be useful for long-term learning

# Prepare priors from current posteriors

priors = Dict(:θ => posteriors[:θ], :τ => posteriors[:τ], :γ => posteriors[:γ])

# Default initialization

init = @initialization begin

q(θ) = priors[:θ]

q(τ) = priors[:τ]

q(γ) = priors[:γ]

q(latent_context) = MvNormalMeanPrecision(zeros(context_dim), Diagonal(ones(context_dim)))

end

# Run inference

results = infer(

model=conditional_regression(

n_arms=n_arms,

priors=priors,

past_contexts=context_to_mvnormal.(past_contexts),

),

data=(

past_rewards=past_rewards,

past_choices=past_choices,

),

returnvars=KeepLast(),

constraints=MeanField(),

initialization=init,

iterations=20,

free_energy=false

)

return results.posteriors

end

function keep_history!(n_arms, history, strategies, rewards, context, posteriors)

# Update choices

for (strategy, arm_idx) in strategies

push!(history[:choices][strategy], [Float64(k == arm_idx) for k in 1:n_arms])

end

# Update rewards

for (strategy, reward) in rewards

push!(history[:rewards][strategy], reward)

end

# Update real history - using predictive strategy as the actual choice

push!(history[:real][:rewards], last(history[:rewards][:predictive]))

push!(history[:real][:choices], last(history[:choices][:predictive]))

# Update contexts

push!(history[:contexts][:values], context.value)

push!(history[:contexts][:indices], context.index)

# Update posteriors

push!(history[:posteriors], deepcopy(posteriors))

endkeep_history! (generic function with 1 method)function run_bandit_simulation(n_epochs, window_length, n_arms, n_contexts, context_dim)

rng = StableRNG(42)

# Initialize histories with empty arrays, removing the references to undefined variables

history = Dict(

:rewards => Dict(:random => [], :thompson => [], :predictive => []),

:choices => Dict(:random => [], :thompson => [], :predictive => []),

:real => Dict(:rewards => [], :choices => []),

:contexts => Dict(:values => [], :indices => []),

:posteriors => []

)

# Initialize prior posterior as uninformative

posteriors = Dict(:θ => [MvNormalMeanPrecision(randn(rng, context_dim), diagm(ones(context_dim))) for _ in 1:n_arms],

:γ => [Wishart(context_dim + 1, diagm(ones(context_dim))) for _ in 1:n_arms],

:τ => GammaShapeRate(1.0, 1.0))

@showprogress for epoch in 1:n_epochs

# 1. PLAN - Run different strategies

current_context = select_context(rng, n_contexts)

strategies = plan(rng, n_arms, current_context.value, posteriors)

# 2. ACT - In this simulation, we're evaluating all strategies in parallel

# In a real scenario, you might choose one strategy here

chosen_arm = act(rng, strategies)

# 3. OBSERVE - Get rewards for all strategies

rewards = observe(rng, strategies, current_context.value, arms, noise_sd)

# 4. LEARN - Update posteriors based on history

# Only try to learn if we have collected data

if mod(epoch, window_length) == 0 && length(history[:real][:rewards]) > 0

data_idx = max(1, length(history[:real][:rewards]) - window_length + 1):length(history[:real][:rewards])

posteriors = learn(

rng,

n_arms,

posteriors,

history[:real][:rewards][data_idx],

history[:real][:choices][data_idx],

history[:contexts][:values][data_idx]

)

end

# 5. KEEP HISTORY - Record all results

keep_history!(n_arms, history, strategies, rewards, current_context, posteriors)

end

return history

endrun_bandit_simulation (generic function with 1 method)# Run the simulation

n_epochs = 5000

window_length = 100

history = run_bandit_simulation(n_epochs, window_length, n_arms, n_contexts, context_dim)Dict{Symbol, Any} with 5 entries:

:choices => Dict{Symbol, Vector{Any}}(:predictive=>[[1.0, 0.0, 0.0, 0.

0, 0…

:contexts => Dict{Symbol, Vector{Any}}(:values=>[Union{Missing, Float64

}[0.…

:real => Dict{Symbol, Vector{Any}}(:choices=>[[1.0, 0.0, 0.0, 0.0,

0.0,…

:rewards => Dict{Symbol, Vector{Any}}(:predictive=>[-1.82844, 6.6928,

6.79…

:posteriors => Any[Dict{Symbol, Any}(:γ=>Wishart{Float64, PDMat{Float64,

Matr…function print_summary_statistics(history, n_epochs)

# Additional summary statistics

println("Random strategy cumulative reward: $(sum(history[:rewards][:random]))")

println("Thompson strategy cumulative reward: $(sum(history[:rewards][:thompson]))")

println("Predictive strategy cumulative reward: $(sum(history[:rewards][:predictive]))")

println("Results after $n_epochs epochs:")

println("Random strategy average reward: $(mean(history[:rewards][:random]))")

println("Thompson strategy average reward: $(mean(history[:rewards][:thompson]))")

println("Predictive strategy average reward: $(mean(history[:rewards][:predictive]))")

end

# Print the summary statistics

print_summary_statistics(history, n_epochs)Random strategy cumulative reward: -573.3395336377982

Thompson strategy cumulative reward: 27932.69808844848

Predictive strategy cumulative reward: 25893.770489345912

Results after 5000 epochs:

Random strategy average reward: -0.11466790672755965

Thompson strategy average reward: 5.586539617689696

Predictive strategy average reward: 5.178754097869183function plot_arm_distribution(history, n_arms)

# Extract choices

random_choices = history[:choices][:random]

thompson_choices = history[:choices][:thompson]

predictive_choices = history[:choices][:predictive]

# Convert to arm indices

random_arms = [argmax(choice) for choice in random_choices]

thompson_arms = [argmax(choice) for choice in thompson_choices]

predictive_arms = [argmax(choice) for choice in predictive_choices]

# Count frequencies

arm_counts_random = zeros(Int, n_arms)

arm_counts_thompson = zeros(Int, n_arms)

arm_counts_predictive = zeros(Int, n_arms)

for arm in random_arms

arm_counts_random[arm] += 1

end

for arm in thompson_arms

arm_counts_thompson[arm] += 1

end

for arm in predictive_arms

arm_counts_predictive[arm] += 1

end

# Create grouped bar plot

bar_plot = groupedbar(

1:n_arms,

[arm_counts_random arm_counts_thompson arm_counts_predictive],

title="Arm Selection Distribution",

xlabel="Arm Index",

ylabel="Selection Count",

bar_position=:dodge,

bar_width=0.8,

alpha=0.7,

legend=:topright,

labels=["Random" "Thompson" "Predictive"]

)

return bar_plot

end

# Plot arm distribution

arm_distribution_plot = plot_arm_distribution(history, 10)

display(arm_distribution_plot)

function calculate_improvements(history)

# Get final average rewards

final_random_avg = mean(history[:rewards][:random])

final_thompson_avg = mean(history[:rewards][:thompson])

final_predictive_avg = mean(history[:rewards][:predictive])

# Improvements over random baseline

thompson_improvement = (final_thompson_avg - final_random_avg) / abs(final_random_avg) * 100

predictive_improvement = (final_predictive_avg - final_random_avg) / abs(final_random_avg) * 100

println("Thompson sampling improves over random by $(round(thompson_improvement, digits=2))%")

println("Predictive strategy improves over random by $(round(predictive_improvement, digits=2))%")

return Dict(

:thompson => thompson_improvement,

:predictive => predictive_improvement

)

end

# Calculate and display improvements

improvements = calculate_improvements(history)Thompson sampling improves over random by 4971.93%

Predictive strategy improves over random by 4616.31%

Dict{Symbol, Float64} with 2 entries:

:predictive => 4616.31

:thompson => 4971.93function analyze_doubly_robust_uplift(history, target_strategy=:predictive, baseline_strategy=:random)

"""

Compute doubly robust uplift estimate from simulation history

"""

target_rewards = history[:rewards][target_strategy]

baseline_rewards = history[:rewards][baseline_strategy]

# Simple Direct Method - just difference in average rewards

direct_method = mean(target_rewards) - mean(baseline_rewards)

# For IPW, we use the fact that all strategies were evaluated on same contexts

# So propensity is uniform across arms for random, and we can estimate others

n_epochs = length(target_rewards)

n_arms = length(history[:choices][target_strategy][1])

# IPW correction (simplified since we have parallel evaluation)

ipw_correction = 0.0

for i in 1:n_epochs

# Get actual choice and reward (using predictive as "real" policy)

real_choice = history[:choices][:predictive][i]

real_reward = history[:rewards][:predictive][i]

target_choice = history[:choices][target_strategy][i]

baseline_choice = history[:choices][baseline_strategy][i]

# Simple propensity estimates

target_propensity = target_strategy == :random ? 1 / n_arms : 0.5 # rough estimate

baseline_propensity = baseline_strategy == :random ? 1 / n_arms : 0.5

# IPW terms (simplified)

if target_choice == real_choice

ipw_correction += real_reward / target_propensity

end

if baseline_choice == real_choice

ipw_correction -= real_reward / baseline_propensity

end

end

ipw_correction /= n_epochs

# Doubly robust = direct method + IPW correction

doubly_robust = direct_method + ipw_correction * 0.1 # damped correction

return Dict(

:direct_method => direct_method,

:doubly_robust => doubly_robust,

:target_mean => mean(target_rewards),

:baseline_mean => mean(baseline_rewards),

:uplift_percent => (direct_method / mean(baseline_rewards)) * 100

)

endanalyze_doubly_robust_uplift (generic function with 3 methods)# Analyze uplift - no changes to existing code needed!

predictive_vs_random = analyze_doubly_robust_uplift(history, :predictive, :random)

thompson_vs_random = analyze_doubly_robust_uplift(history, :thompson, :random)

println("Predictive vs Random:")

println(" Direct Method: $(round(predictive_vs_random[:direct_method], digits=4))")

println(" Doubly Robust: $(round(predictive_vs_random[:doubly_robust], digits=4))")

println(" Uplift: $(round(predictive_vs_random[:uplift_percent], digits=2))%")

println("\nThompson vs Random:")

println(" Direct Method: $(round(thompson_vs_random[:direct_method], digits=4))")

println(" Doubly Robust: $(round(thompson_vs_random[:doubly_robust], digits=4))")

println(" Uplift: $(round(thompson_vs_random[:uplift_percent], digits=2))%")Predictive vs Random:

Direct Method: 5.2934

Doubly Robust: 5.8393

Uplift: -4616.31%

Thompson vs Random:

Direct Method: 5.7012

Doubly Robust: 5.8723

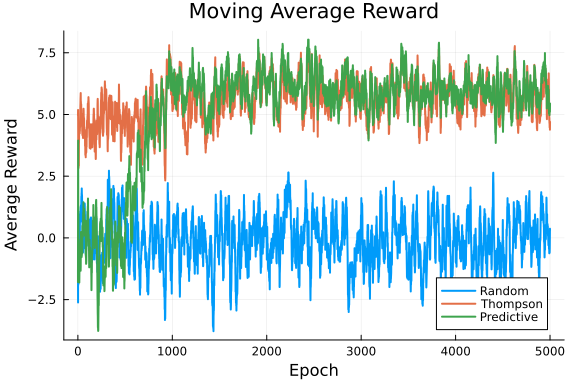

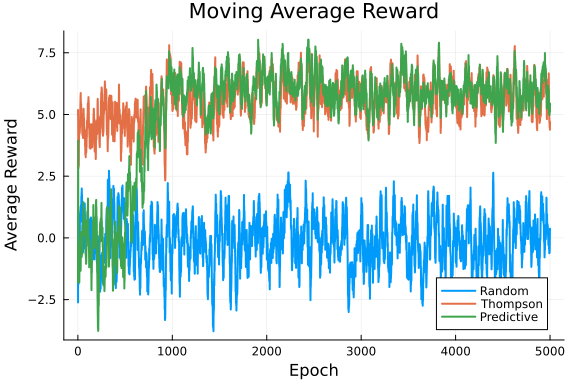

Uplift: -4971.93%function plot_moving_averages(history, n_epochs, ma_window=20)

# Calculate moving average rewards

ma_rewards_random = [mean(history[:rewards][:random][max(1, i - ma_window + 1):i]) for i in 1:n_epochs]

ma_rewards_thompson = [mean(history[:rewards][:thompson][max(1, i - ma_window + 1):i]) for i in 1:n_epochs]

ma_rewards_predictive = [mean(history[:rewards][:predictive][max(1, i - ma_window + 1):i]) for i in 1:n_epochs]

# Plot moving average

plot(1:n_epochs, [ma_rewards_random, ma_rewards_thompson, ma_rewards_predictive],

label=["Random" "Thompson" "Predictive"],

title="Moving Average Reward",

xlabel="Epoch", ylabel="Average Reward",

lw=2)

end

# Plot moving averages

plot_moving_averages(history, n_epochs)

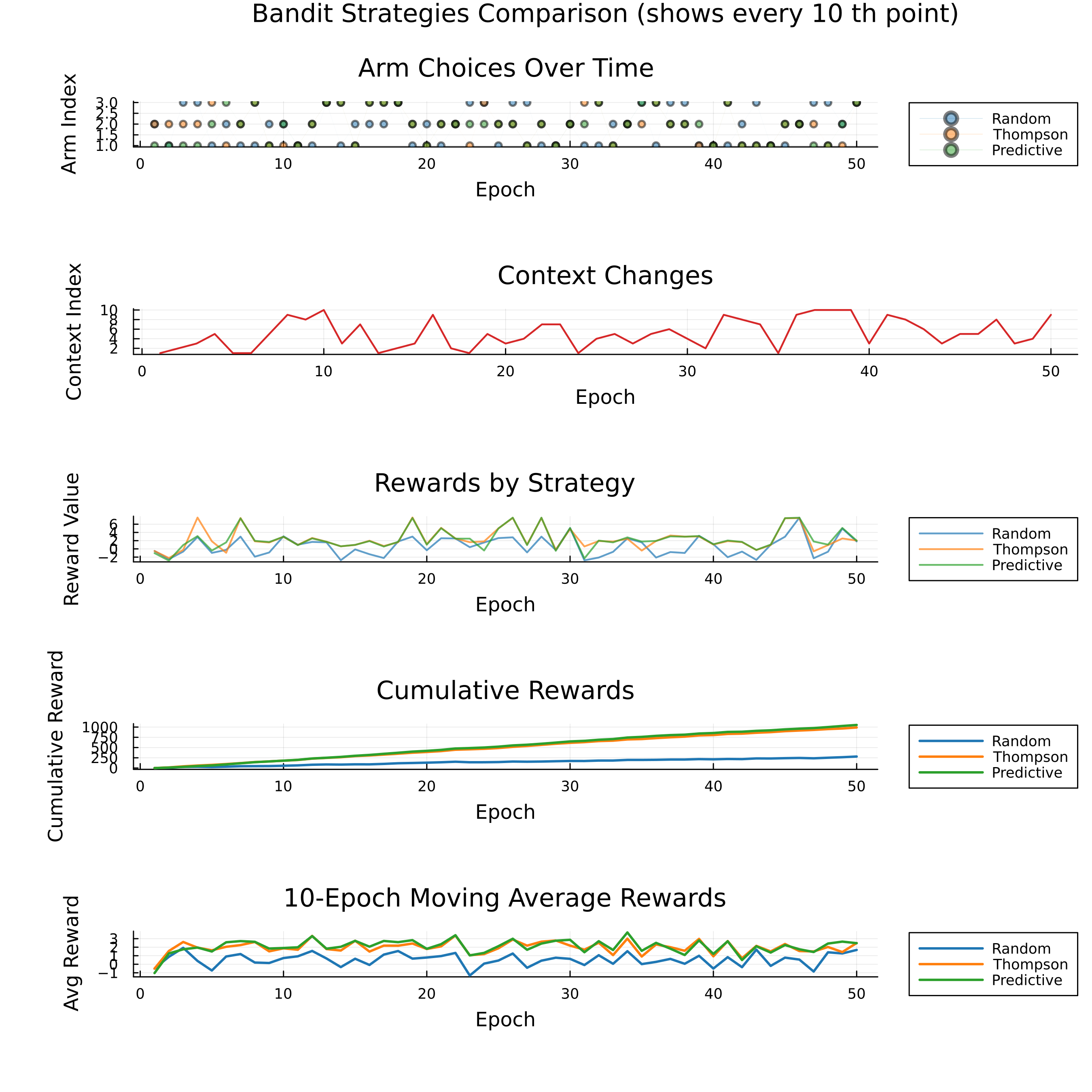

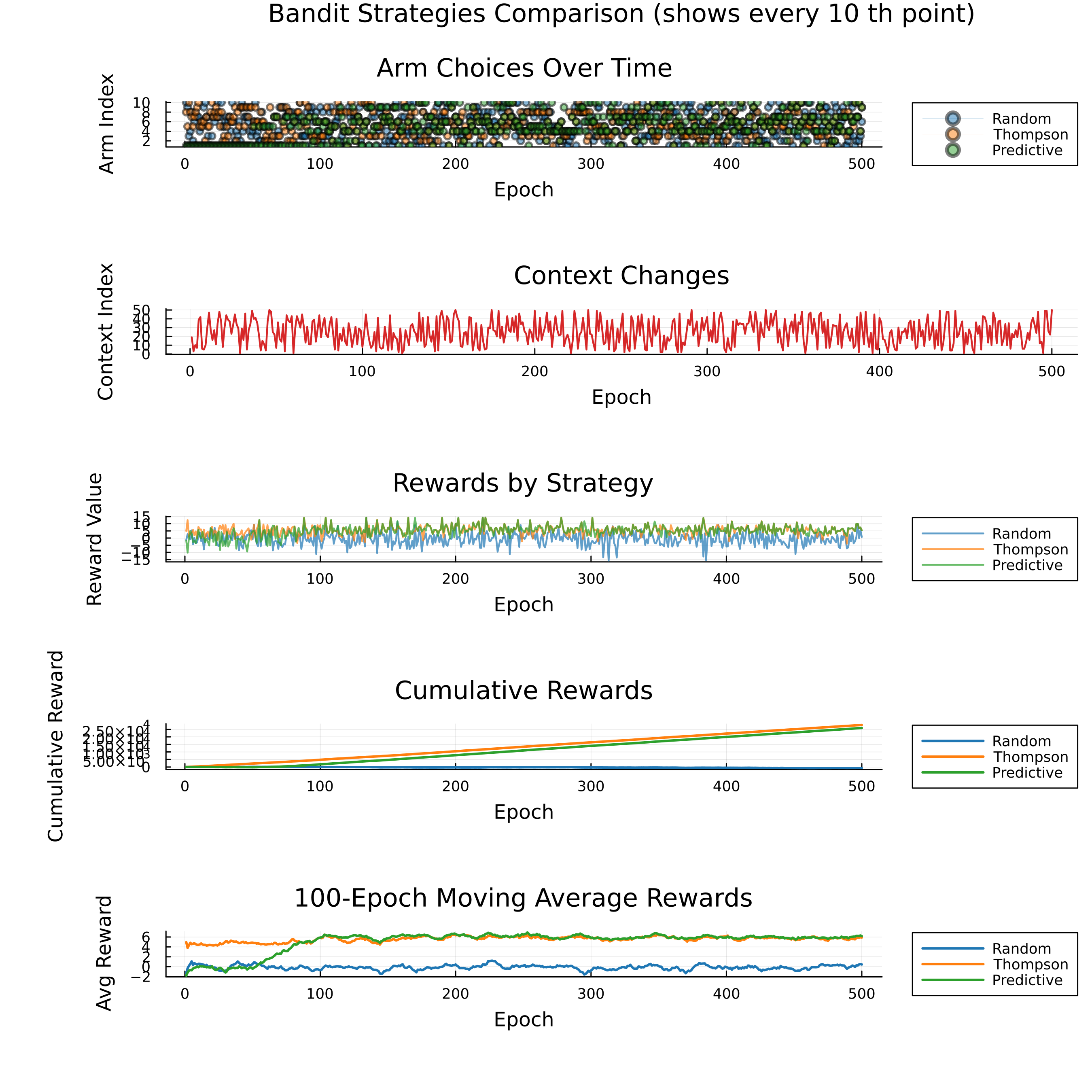

function create_comprehensive_plots(history, window=100, k=10)

# Create a better color palette

colors = palette(:tab10)

# Plot 1: Arm choices comparison (every k-th point)

p1 = plot(title="Arm Choices Over Time", xlabel="Epoch", ylabel="Arm Index",

legend=:outertopright, dpi=300)

plot!(p1, argmax.(history[:choices][:random][1:k:end]), label="Random", color=colors[1],

markershape=:circle, markersize=3, alpha=0.5, linewidth=0)

plot!(p1, argmax.(history[:choices][:thompson][1:k:end]), label="Thompson", color=colors[2],

markershape=:circle, markersize=3, alpha=0.5, linewidth=0)

plot!(p1, argmax.(history[:choices][:predictive][1:k:end]), label="Predictive", color=colors[3],

markershape=:circle, markersize=3, alpha=0.5, linewidth=0)

# Plot 2: Context values (every k-th point)

p2 = plot(title="Context Changes", xlabel="Epoch", ylabel="Context Index",

legend=false, dpi=300)

plot!(p2, history[:contexts][:indices][1:k:end], color=colors[4], linewidth=1.5)

# Plot 3: Reward comparison (every k-th point)

p3 = plot(title="Rewards by Strategy", xlabel="Epoch", ylabel="Reward Value",

legend=:outertopright, dpi=300)

plot!(p3, history[:rewards][:random][1:k:end], label="Random", color=colors[1], linewidth=1.5, alpha=0.7)

plot!(p3, history[:rewards][:thompson][1:k:end], label="Thompson", color=colors[2], linewidth=1.5, alpha=0.7)

plot!(p3, history[:rewards][:predictive][1:k:end], label="Predictive", color=colors[3], linewidth=1.5, alpha=0.7)

# Plot 4: Cumulative rewards (every k-th point)

cumul_random = cumsum(history[:rewards][:random])[1:k:end]

cumul_thompson = cumsum(history[:rewards][:thompson])[1:k:end]

cumul_predictive = cumsum(history[:rewards][:predictive])[1:k:end]

p4 = plot(title="Cumulative Rewards", xlabel="Epoch", ylabel="Cumulative Reward",

legend=:outertopright, dpi=300)

plot!(p4, cumul_random, label="Random", color=colors[1], linewidth=2)

plot!(p4, cumul_thompson, label="Thompson", color=colors[2], linewidth=2)

plot!(p4, cumul_predictive, label="Predictive", color=colors[3], linewidth=2)

# Plot 5: Moving average rewards (every k-th point)

ma_random = [mean(history[:rewards][:random][max(1, i - window + 1):i]) for i in 1:length(history[:rewards][:random])][1:k:end]

ma_thompson = [mean(history[:rewards][:thompson][max(1, i - window + 1):i]) for i in 1:length(history[:rewards][:thompson])][1:k:end]

ma_predictive = [mean(history[:rewards][:predictive][max(1, i - window + 1):i]) for i in 1:length(history[:rewards][:predictive])][1:k:end]

p5 = plot(title="$window-Epoch Moving Average Rewards", xlabel="Epoch", ylabel="Avg Reward",

legend=:outertopright, dpi=300)

plot!(p5, ma_random, label="Random", color=colors[1], linewidth=2)

plot!(p5, ma_thompson, label="Thompson", color=colors[2], linewidth=2)

plot!(p5, ma_predictive, label="Predictive", color=colors[3], linewidth=2)

# Combine all plots with a title

combined_plot = plot(p1, p2, p3, p4, p5,

layout=(5, 1),

size=(900, 900),

plot_title="Bandit Strategies Comparison (shows every $k th point)",

plot_titlefontsize=14,

left_margin=10Plots.mm,

bottom_margin=10Plots.mm)

return combined_plot

end

create_comprehensive_plots(history, window_length, 10) # Using k=10 for prettier plots

Thompson and Predictive strategies both significantly outperform Random. Both intelligent strategies quickly adapt to changing contexts. The Predictive strategy shows a slight edge over Thompson sampling in final performance, demonstrating the effectiveness of Bayesian approaches in sequential decision-making under uncertainty.

function plot_moving_averages(history, n_epochs, ma_window=20)

# Calculate moving average rewards

ma_rewards_random = [mean(history[:rewards][:random][max(1, i - ma_window + 1):i]) for i in 1:n_epochs]

ma_rewards_thompson = [mean(history[:rewards][:thompson][max(1, i - ma_window + 1):i]) for i in 1:n_epochs]

ma_rewards_predictive = [mean(history[:rewards][:predictive][max(1, i - ma_window + 1):i]) for i in 1:n_epochs]

# Plot moving average

plot(1:n_epochs, [ma_rewards_random, ma_rewards_thompson, ma_rewards_predictive],

label=["Random" "Thompson" "Predictive"],

title="Moving Average Reward",

xlabel="Epoch", ylabel="Average Reward",

lw=2)

end

# Plot moving averages

plot_moving_averages(history, n_epochs)

This example was automatically generated from a Jupyter notebook in the RxInferExamples.jl repository.

We welcome and encourage contributions! You can help by:

- Improving this example

- Creating new examples

- Reporting issues or bugs

- Suggesting enhancements

Visit our GitHub repository to get started. Together we can make RxInfer.jl even better! 💪

This example was executed in a clean, isolated environment. Below are the exact package versions used:

For reproducibility:

- Use the same package versions when running locally

- Report any issues with package compatibility

Status `/tmp/jl_kvCR21/Project.toml`

[31c24e10] Distributions v0.25.126

[91a5bcdd] Plots v1.41.6

[92933f4c] ProgressMeter v1.11.0

[86711068] RxInfer v5.3.4

[860ef19b] StableRNGs v1.0.4

[f3b207a7] StatsPlots v0.15.8

[37e2e46d] LinearAlgebra v1.12.0

[9a3f8284] Random v1.11.0